"Tuesday, Jan 16, 2024 - 08:10 AM

By John Kemp, senior market analyst at Reuters

Portfolio investors purchased petroleum in the first full week of 2024, reversing sales the previous week and continuing the pattern of choppy trading that has continued since early December.

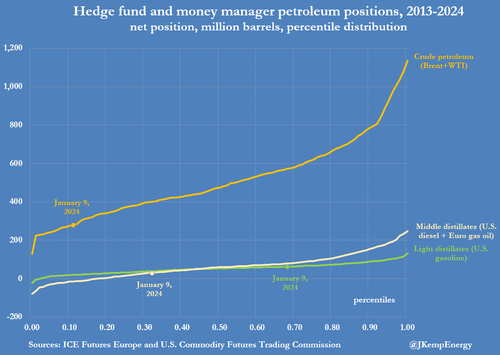

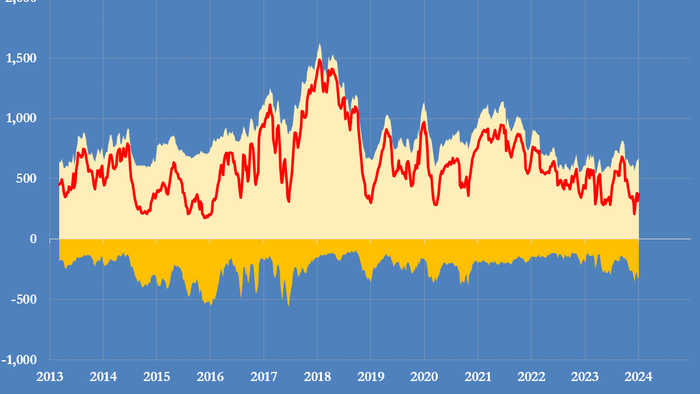

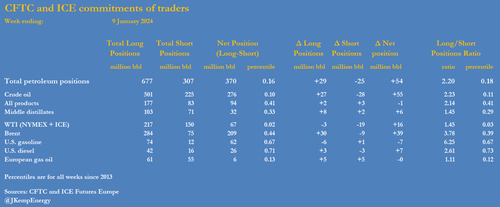

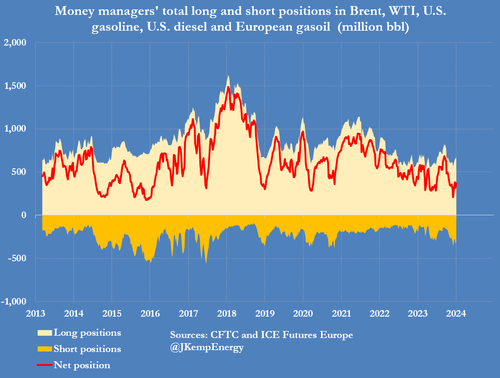

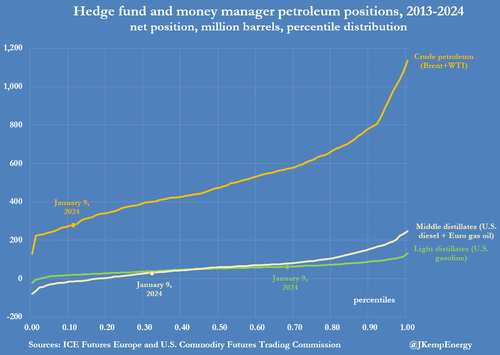

Hedge funds and other money managers bought the equivalent of 54 million barrels in the six most important petroleum futures and options contracts over the seven days ending on January 9.

Purchases largely reversed sales of 66 million barrels the previous week, according to records filed with ICE Futures Europe and the U.S. Commodity Futures Trading Commission.

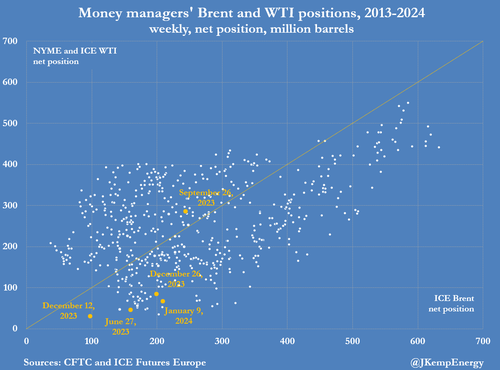

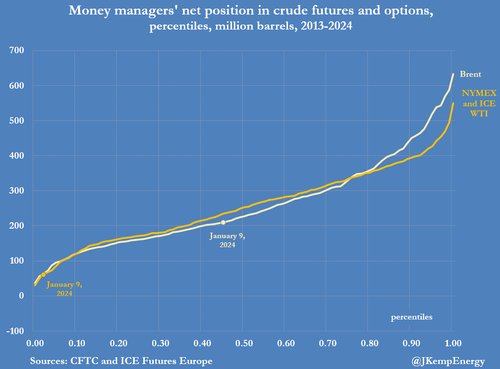

In the most recent week, purchases focused on crude (+55 million barrels) reversing the previous week’s crude-dominated sales (-63 million).

There were only minor adjustments in U.S. gasoline (+7 million barrels), U.S. diesel (-7 million) and European gas oil (no change). Despite some position volatility, the basic picture has remained the same since early December.

Fund managers have been strongly bullish on refined fuels in the United States owing to relatively low inventories and healthy outlook for the economy and fuel consumption.

Funds have been neutral about Brent with plentiful inventories and new sources of supply offset by OPEC⁺ production cuts and the threat of disruption to export routes from conflict in the Red Sea.

But the hedge fund community has been outright bearish about WTI with plentiful crude inventories in the United States and persistent growth in production from shale producers.

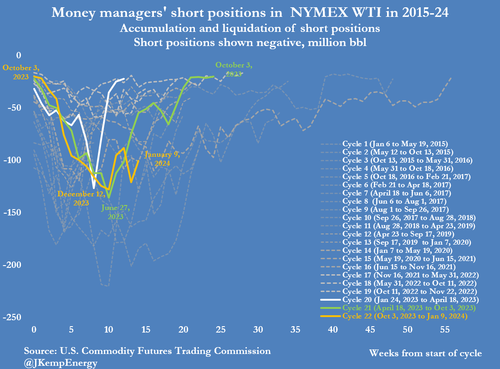

There was some short-covering in the premier NYMEX WTI contract with short positions reduced by 20 million barrels in the most recent week. But remaining short positions are still elevated at 101 million barrels.

From a positioning perspective, there is a significant risk that further short-covering will fuel a sharp rally in WTI prices.

Yet most managers are convinced the fundamentals remain poor with production set to outstrip consumption ensuring prices fall first.

U.S. NATURAL GAS

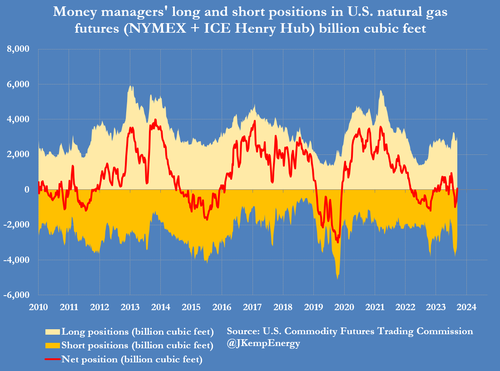

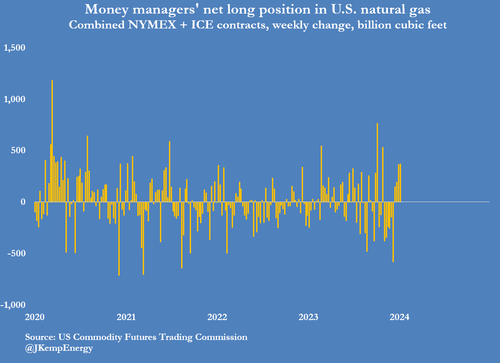

Investors are becoming less bearish about the outlook for gas prices in the United States as production growth slows.

Hedge funds and other money managers purchased the equivalent of 369 billion cubic feet (bcf) of gas in the two major futures and options contracts over the seven days ending on January 9.

Funds have bought a total of 1,078 bcf over the most recent four weeks, which was the fastest rate of buying since the middle of 2021.

In consequence, funds had built a net long position of 80 bcf (35th percentile for all weeks since 2010) by January 9 up from a net short of 999 bcf (8th percentile) on December 12.

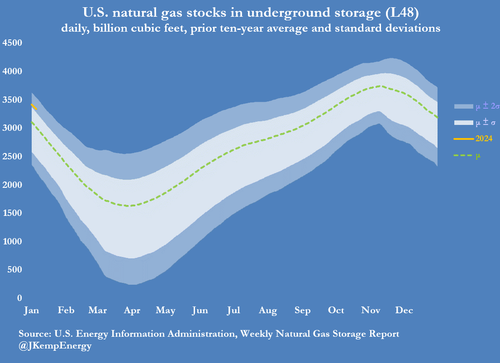

Working gas inventories were still 320 bcf (+11% or +1.21 standard deviations) above the prior 10-year seasonal average on January 5, the highest for the time of year since 2016.

The surplus had swelled from 60 bcf (+2% or +0.23 standard deviations) near the start of the winter season on October 6.

But production growth had slowed to less than 3% per year by August-October 2023 from more than 6% a year earlier.

Production gains have slowed in response to the sharp fall in prices since mid-2022 and the slowdown is set to deepen into early 2024.

Front-month futures prices have averaged just below $3 per million British thermal units so far in January 2024, which puts them in only the 10th percentile for all months since the start of the century, after adjusting for inflation.

With prices already low and production growth slowing, fund managers are becoming much less bearish on gas prices, even if outright bullishness remains rare at this point."